Oct03

For too long, climate change has been framed as an abstract moral crusade, a question of belief or politics. But business leaders and policymakers don’t get to operate in the world of abstraction. They run companies, ministries, and economies in the material world, where physical assets get destroyed, balance sheets wobble, and financial systems seize up when unmanaged risk compounds.

The brutal truth is this: climate change is first and foremost a risk management challenge. And like all risks, it can’t be eliminated, but it can be priced, prioritised, mitigated, and prepared for.

That was the framing offered by economist Gary Yohe, one of the architects of the IPCC’s shift from cost–benefit calculus to iterative risk management. Yohe has a way of distilling it to a stark but useful triad: abate, adapt, or suffer. That’s not a slogan. It’s the unavoidable choice set. Every tonne of emissions we cut lowers the risk of catastrophic events. Every euro or dollar invested in resilience reduces the impact when those events still occur. Whatever we don’t abate or adapt to, we will simply have to absorb - as loss, as disruption, as social fracture.

the signals are already everywhere.

These aren’t activist talking points. They’re actuarial decisions. If the insurers, society’s professional risk managers, are pricing climate change as uninsurable, then boards and cabinets must take the hint.

Executives and politicians need to think about climate risk the way central banks do: by classifying it into buckets that can be monitored and managed.

1. Physical risks.

These are the acute shocks (storms, wildfires, floods, heatwaves) and chronic drags (sea level rise, water stress, permafrost thaw) that hit infrastructure, assets, and people. NOAA’s records show billion-dollar disasters in the US have quadrupledin frequency since the 1980s. Europe is no better: the EEA warns the cost curve will keep rising unless adaptation accelerates.

2. Transition risks.

Markets and regulations are moving. The EU’s Corporate Sustainability Reporting Directive (CSRD) and the global IFRS S2 climate disclosure baseline make scenario analysis and risk integration non-negotiable. Companies that lag will face higher capital costs, eroding market share, or both.

3. Liability risks.

Litigation is now a climate risk vector. As disclosure frameworks tighten, directors and officials who fail to account for foreseeable climate risk could be held accountable, in court.

The Allianz Group recently put it bluntly: “Our goal is to keep the world insurable. But we cannot do it alone.” Their July 2025 climate risk report warns that only about one-third of natural disaster losses are insured, and the gap between insured and uninsured losses is growing faster than coverage can keep up .

This is not just an insurance industry headache. When coverage disappears:

Allianz’s conclusion is stark: beyond 3°C of warming, vast areas could become “effectively uninsurable”, leaving states unable to cover the residual costs . That’s systemic risk, the kind that crashes economies. In fact, they warn that the worsening climate crisis could ultimately destroy capitalism. Strong language from an industry as risk averse as insurance.

The financial system is treating climate as core business risk. Boards and ministries that lag are exposed.

If finance is embedding climate into enterprise risk management and capital planning, so must operating companies and governments.

Treating climate as risk management reframes adaptation. It isn’t charity. It’s corporate finance.

The World Bank estimates $4 in benefits for every $1 invested in resilient infrastructure. The Global Commission on Adaptation projected that $1.8 trillion in resilience investment by 2030 could generate $7.1 trillion in net benefits - through avoided losses, higher productivity, and co-benefits like healthier crops and cleaner water.

Allianz models the same dual-front strategy: mitigation to cap future risks, and adaptation to blunt unavoidable impacts . They’ve committed €170 billion to sustainable investments, from offshore wind to green hydrogen, while still underwriting resilience upgrades for clients. That’s not activism. That’s balance-sheet protection.

Supply chains turn climate hazards into systemic shocks. Consider the 2011 Thailand floods: factories producing 40% of the world’s hard disk drives were submerged, sending global IT hardware supply into chaos for months. Japanese automakers lost hundreds of thousands of units as suppliers sat underwater.

Fast forward: drought in the Panama Canal has already throttled global shipping. A hotter, wetter, more chaotic world means supply networks will face serial disruptions. For business leaders, the lesson is clear: map supplier exposure, build redundancy where critical inputs cluster in risk-prone regions, and bake climate resilience into procurement.

So what does a serious climate risk management agenda look like? Ten moves:

For governments, the most effective interventions look less like slogans and more like risk engineering:

Here’s where Gary Yohe’s distinction matters. Optimism says it will all turn out fine. Hope says action makes sense, even when outcomes are uncertain. That’s the stance leaders need.

Vaclav Havel put it best: hope is “the certainty that something makes sense, regardless of how it turns out.” It’s that certainty which keeps mayors upgrading flood defences, keeps CFOs building resilience lines into budgets, keeps policymakers pushing emissions limits through legislatures.

And it’s not naïve. It’s pragmatic. Leaders don’t need perfect certainty to act. Central banks, insurers, and statistical agencies have already given us enough signal. The choice now is whether to act with foresight, or pay later in compound losses.

Climate change isn’t a morality tale. It’s a risk ledger. And the arithmetic is merciless: every risk not abated must be adapted to, and every risk not adapted to will be suffered. The good news is that the toolkit exists. The return on resilience is positive. And the cost of delay is rising.

The insurance sector has already sounded the alarm. Allianz’s blunt assessment, that entire regions could become uninsurable if we don’t change course, should be ringing in every boardroom and cabinet office.

For leaders, the imperative is clear: treat climate like any other systemic risk. Set thresholds, allocate capital, monitor exposures, build resilience, and move. Hope, not blind optimism, should fuel the work.

If this resonates, you’ll want to hear the full conversation I had with Professor Gary Yohe on the Climate Confident Podcast. We unpack the abate–adapt–suffer triad, the limits of insurance, and what risk management really looks like in a climate-stressed world.

Photo credit Glenn Beltz on Flickr

This post was originally posted on TomRaftery.com

By Tom Raftery

Keywords: Climate Change, Risk Management, Sustainability

The borders have moved, and leadership has not yet caught up

The borders have moved, and leadership has not yet caught up No More Hold Music: How AI is Fixing the UK’s Customer Service Crisis

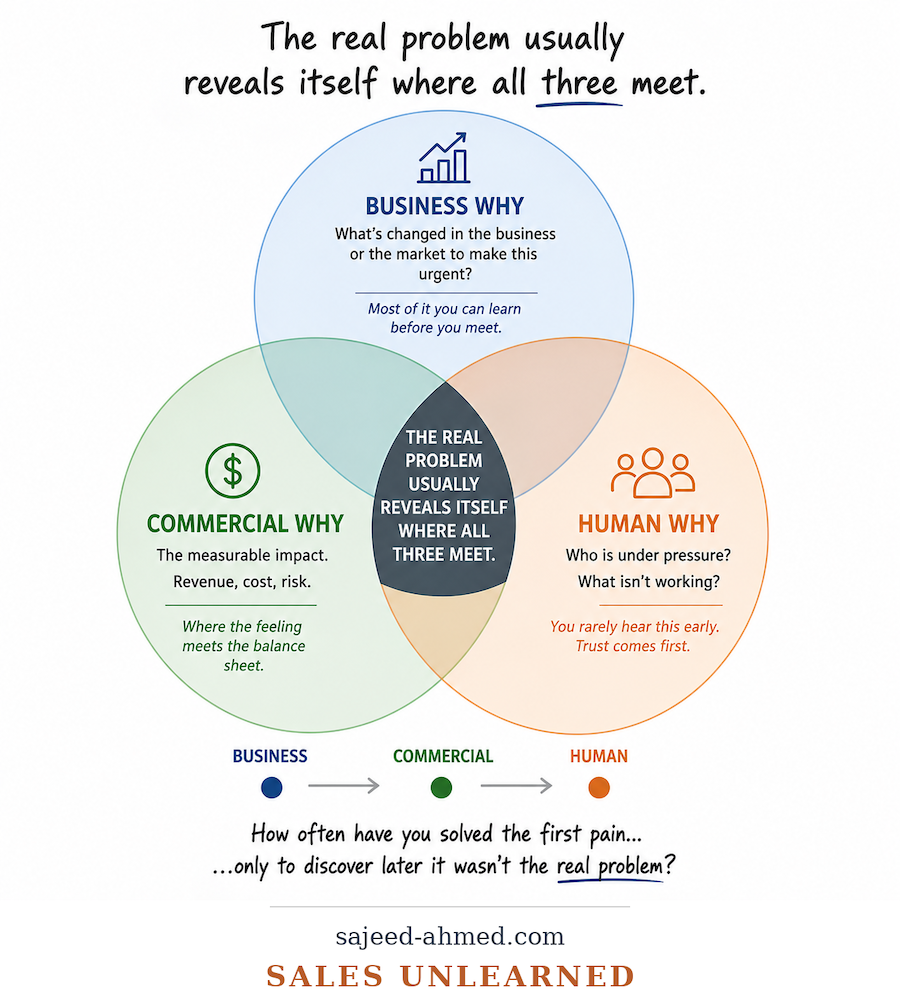

No More Hold Music: How AI is Fixing the UK’s Customer Service Crisis Why the First Customer Pain Is Rarely the Real Problem in Enterprise Sales

Why the First Customer Pain Is Rarely the Real Problem in Enterprise Sales The Missing Middle: Why Privately Held Companies Have Lost Their Mid-Career Talent

The Missing Middle: Why Privately Held Companies Have Lost Their Mid-Career Talent When Products Can't Reach the Market

When Products Can't Reach the Market