Influencer, Thought Leader, and Storyteller focusing on Sustainability, Supply Chain, and Technology

Available For: Advising, Authoring, Consulting, Influencing, Speaking

Travels From: Spain

Speaking Topics: Sustainability, Supply Chain, Energy Transition,

| Tom Raftery | Points |

|---|---|

| Academic | 0 |

| Author | 2395 |

| Influencer | 393 |

| Speaker | 90 |

| Entrepreneur | 10 |

| Total | 2888 |

Points based upon Thinkers360 patent-pending algorithm.

Tags: AI, Sustainability, Supply Chain

Tags: AI, Sustainability, Supply Chain

Bad Emissions Data Is Now a Supply Chain Risk

Bad Emissions Data Is Now a Supply Chain Risk

Tags: AI, Supply Chain, Sustainability

Tags: AI, Sustainability, Supply Chain

Tags: AI, Sustainability, Supply Chain

Tags: AI, Sustainability, Supply Chain

Tags: AI, Sustainability, Supply Chain

Tags: AI, Sustainability, Supply Chain

Energy System Resilience: Lessons Europe Must Learn from Ukraine

Energy System Resilience: Lessons Europe Must Learn from Ukraine

Tags: IoT, Supply Chain, Sustainability

Capital Follows Electrons: How Electrification Is Driving Growth

Capital Follows Electrons: How Electrification Is Driving Growth

Tags: IoT, Supply Chain, Sustainability

Building Decarbonisation Is No Longer Optional. It’s Strategic.

Building Decarbonisation Is No Longer Optional. It’s Strategic.

Tags: IoT, Supply Chain, Sustainability

Why Poor ESG Data Is Now a Business Liability

Why Poor ESG Data Is Now a Business Liability

Tags: IoT, Supply Chain, Sustainability

When the Grid Became the Risk: Why Businesses Are Turning to Solar + Storage PPAs

When the Grid Became the Risk: Why Businesses Are Turning to Solar + Storage PPAs

Tags: IoT, Supply Chain, Sustainability

Tags: AI, Sustainability, Supply Chain

Solar’s Second Sunrise: Why the Next Decade Will Outshine Everything We’ve Seen So Far

Solar’s Second Sunrise: Why the Next Decade Will Outshine Everything We’ve Seen So Far

Tags: IoT, Supply Chain, Sustainability

Scope 3 Is About to Redraw the Corporate Map: And Companies Serving Fossil Fuels Are Standing on a Fault Line

Scope 3 Is About to Redraw the Corporate Map: And Companies Serving Fossil Fuels Are Standing on a Fault Line

Tags: IoT, Supply Chain, Sustainability

When One Scanner Fails: Why Resilience Starts at the Smallest Link

When One Scanner Fails: Why Resilience Starts at the Smallest Link

Tags: IoT, Supply Chain, Sustainability

Why Scope 3 Data Starts in the Dark – and How Food Brands Are Showing the Way Out

Why Scope 3 Data Starts in the Dark – and How Food Brands Are Showing the Way Out

Tags: IoT, Supply Chain, Sustainability

Tags: AI, Sustainability, Supply Chain

Why You Can’t Drone a Solar Panel: Electrification and Europe’s New Energy Security

Why You Can’t Drone a Solar Panel: Electrification and Europe’s New Energy Security

Tags: IoT, Supply Chain, Sustainability

Why Decarbonising Power Is the 21st-Century Economic Upgrade We Can’t Afford to Delay

Why Decarbonising Power Is the 21st-Century Economic Upgrade We Can’t Afford to Delay

Tags: IoT, Supply Chain, Sustainability

Tags: AI, Sustainability, Supply Chain

Tags: AI, Sustainability, Supply Chain

Big Tech, Big Promises, Bigger Emissions: The Truth About Corporate Climate Claims

Big Tech, Big Promises, Bigger Emissions: The Truth About Corporate Climate Claims

Tags: AI, Supply Chain, Sustainability

Tags: AI, Sustainability, Supply Chain

2 Terawatts of Solar Power, Electric Mining Trucks, and the Future of ESG: Sustainability's Big Moves

2 Terawatts of Solar Power, Electric Mining Trucks, and the Future of ESG: Sustainability's Big Moves

Tags: IoT, Supply Chain, Sustainability

AI Takes Over: Nobel Prizes, Clean Energy, and Supply Chain Wins

AI Takes Over: Nobel Prizes, Clean Energy, and Supply Chain Wins

Tags: IoT, Supply Chain, Sustainability

Executive Fellow

Executive Fellow

Tags: Business Strategy, Leadership, Manufacturing

Tags: AI, Autonomous Vehicles, Sustainability

Tags: Digital Transformation, HealthTech, IoT

Tags: AI, Blockchain, Digital Transformation

Tags: Digital Disruption, Digital Transformation, Innovation

Tags: Digital Disruption, Digital Transformation, Emerging Technology

Tags: Digital Disruption, Digital Transformation, Emerging Technology

Tags: Digital Disruption, Emerging Technology, IoT

Tags: Digital Transformation, IoT, Sustainability

Tags: Digital Transformation, Emerging Technology, IoT

Tags: Future of Work, HR, Sustainability

Tags: Cloud, Digital Transformation, IoT

Tags: Digital Transformation, Emerging Technology, IoT

IOT’S ECOSYSTEM OF TECHNOLOGY WITH TOM RAFTERY OF SAP

IOT’S ECOSYSTEM OF TECHNOLOGY WITH TOM RAFTERY OF SAP

Tags: AI, Blockchain, Emerging Technology, IoT

What will the world look like 10 years from now?

What will the world look like 10 years from now?

Tags: Digital Disruption, Digital Transformation, Emerging Technology

Tags: Cybersecurity, Digital Transformation, IoT

Tom Raftery: "In ten years technology will have transformed the world"

Tom Raftery: "In ten years technology will have transformed the world"

Tags: Digital Transformation, HealthTech, Mobility

Tags: Digital Transformation, Emerging Technology, Innovation

Tags: Digital Disruption, Innovation, IoT

Tags: Emerging Technology, Innovation, IoT

Tags: Emerging Technology, Innovation, IoT

Tags: Cybersecurity, Digital Transformation, IoT

Digital disruption driving force behind 4th industrial revolution

Digital disruption driving force behind 4th industrial revolution

Tags: Digital Transformation, Emerging Technology, IoT

Tags: IoT, Supply Chain

Tags: IoT, Supply Chain

Tags: IoT, Supply Chain

Tags: IoT, Supply Chain

Tags: IoT, Supply Chain

Tags: IoT, Supply Chain

Tags: IoT, Supply Chain, Retail

Tags: IoT, Supply Chain

Tags: IoT, Supply Chain

Tags: IoT, Supply Chain

Tags: IoT, Supply Chain

Tags: IoT, Supply Chain

Tags: IoT, Supply Chain

Tags: IoT, Supply Chain

Tags: IoT, Supply Chain

Tags: IoT, Supply Chain

Tags: IoT, Supply Chain

Tags: IoT, Supply Chain

Tags: IoT, Supply Chain

Tags: IoT, Supply Chain

Tags: IoT, Supply Chain

Tags: IoT, Supply Chain

Tags: IoT, Supply Chain, Sustainability

Tags: IoT, Supply Chain

Tags: IoT, Supply Chain

Tags: IoT, Renewable Energy

Date : October 21, 2024

Date : December 06, 2023

Date : October 24, 2023

Carbon Data Is Becoming Permission to Sell

Carbon Data Is Becoming Permission to Sell

A few years ago, if a company had poor carbon data, the worst-case outcome was often embarrassment.

A weak ESG report.

A few awkward investor questions.

Maybe a raised eyebrow from procurement.

A consultant hired. A dashboard built. A target announced. Everyone went home feeling faintly virtuous.

That world is ending.

Increasingly, poor climate data will not just make a company look bad. It may make products harder to sell, harder to insure, harder to finance, harder to import, and harder to defend in front of regulators, customers, and investors.

This was the line that stayed with me from my recent Climate Confident conversation with Stephen Jamieson, Chief Marketing Officer for SAP Sustainability. Stephen made a deceptively simple point: if companies cannot meet emerging carbon data and product compliance conditions, they may simply not be able to put certain products on the market. He was talking about digital product passports, product carbon footprints, CBAM, metals, fashion, and the rising granularity of carbon data needed just to do business.

That is the shift.

Carbon data is moving from reporting obligation to commercial operating condition.

And for senior leaders, that changes everything.

Let’s start with the policy stack, because this is not about one regulation, one disclosure framework, or one enthusiastic sustainability team trying to get procurement to return its calls.

The EU Carbon Border Adjustment Mechanism, or CBAM, entered its definitive regime on 1 January 2026. EU importers of covered goods now need to declare embedded emissions and surrender the corresponding number of CBAM certificates each year, with authorised declarant status becoming central to compliance.

Translation: carbon is becoming part of the cost of crossing a border.

Then there is the Ecodesign for Sustainable Products Regulation, or ESPR. The European Commission’s 2025-2030 working plan prioritises steel and aluminium, textiles, furniture, tyres, mattresses, and energy-related products for future ecodesign and energy labelling measures. Digital Product Passports sit inside this agenda, turning product sustainability from a nice brochure into structured, exchangeable product data. The QR code is not the strategy. The data behind it is.

Batteries show where this is heading. The EU Batteries Regulation takes a full life-cycle approach, covering sourcing, manufacturing, use, and recycling. From 2025, it gradually introduces carbon footprint declarations, performance classes, and maximum carbon footprint limits for electric vehicle batteries, light means of transport batteries, and rechargeable industrial batteries. It also provides for QR-code access to a digital battery passport with detailed product information.

Packaging is joining the queue too. The Packaging and Packaging Waste Regulation entered into force in February 2025and will generally apply from August 2026. It covers all packaging and packaging waste, regardless of material or origin, and aims to make all packaging on the EU market recyclable in an economically viable way by 2030.

And this is broader than carbon. The EU Deforestation Regulation applies from 30 December 2026 for large and medium operators, requiring covered products to be deforestation-free. The EU Forced Labour Regulation will ban products made with forced labour from being sold in the EU market from 14 December 2027, applying to imports, EU-made products, and exports.

Different rules. Same direction.

Prove it.

At the same time, finance is tightening the lens. IFRS S2, effective for annual reporting periods beginning on or after 1 January 2024, requires companies to disclose climate-related risks and opportunities that could affect cash flows, access to finance, or cost of capital over the short, medium, or long term.

This is where the neat old boundary between “sustainability” and “business” collapses. Bad climate data is no longer just a disclosure gap. It is a pricing gap. A risk gap. A market-access gap.

The same pressure is visible in the voluntary and industry-led space. WBCSD’s Partnership for Carbon Transparency, or PACT, says supply chains cannot decarbonise without accurate and comparable product-level data, and its methodology is built around supplier-specific primary data for product carbon footprints.

Averages got us started.

They will not get us through this next phase.

The implications are enormous, and not in the abstract “ESG is important” way that makes executives reach for their phones.

This is about product viability.

A company may still be able to manufacture a product. It may still have demand. It may still have a strong brand, loyal customers, and a procurement team that thinks it has things under control. But if the company cannot provide credible data on embedded carbon, recycled content, deforestation risk, packaging compliance, forced labour exposure, or product-level sustainability attributes, its commercial freedom narrows.

That is a different conversation.

It means sustainability data becomes part of revenue protection.

Procurement will need to know it.

Finance will need to trust it.

Operations will need to act on it.

Product teams will need to design with it.

AI systems will need to optimise around it.

This last point is crucial.

Stephen made a point in the episode that should make every AI-happy boardroom pause. Businesses are very good at measuring cost, revenue, utilisation, and finance. So AI will optimise for those high-quality inputs. If carbon, water, recycled content, resilience, and wider sustainability factors are not in the same decision environment, they risk becoming secondary, or worse, optimised against.

That is the danger.

AI will not wake up one morning with a conscience. It will optimise for what the system tells it to value.

So if sustainability data lives in a side platform, updated annually, disconnected from ERP, procurement, product lifecycle management, finance, and supply chain planning, then we should not be surprised when automated decisions accelerate the wrong outcomes.

Efficient nonsense is still nonsense.

There is an affordability angle here too. Clean technology is already pulling capital at scale. According to the IEA’s World Energy Investment 2025 report, global energy investment was set to reach USD 3.3 trillion in 2025, with around USD 2.2 trillion going to renewables, nuclear, grids, storage, low-emissions fuels, efficiency, and electrification, twice the USD 1.1 trillion going to oil, gas, and coal.

Capital is moving.

But capital follows confidence. And confidence follows data.

If a company can prove that its product has lower embedded emissions, lower exposure to carbon-intensive inputs, stronger traceability, and better compliance readiness, that is no longer just a sustainability claim. It is commercial differentiation.

So what should leaders do?

First, stop treating climate data as an annual reporting project. That model is too slow, too blunt, and too disconnected from the decisions that matter.

Start with a product exposure map. Which products rely on CBAM-covered materials? Which products fall into ESPR priority sectors? Which use packaging exposed to PPWR? Which contain batteries? Which touch commodities covered by deforestation rules? Which depend on suppliers in high-risk labour regions?

This is not box-ticking. It is revenue risk analysis.

Second, build what I would call a climate-data bill of materials. For priority products, companies need to know the materials, suppliers, production sites, energy inputs, packaging, recycled content, logistics, emissions factors, primary data availability, and evidence gaps.

Boring? Maybe.

Vital? Absolutely.

Third, put procurement in the middle of this. Supplier climate data cannot remain a favour requested politely by sustainability teams once a year. It needs to be built into supplier onboarding, contracts, scorecards, renewal criteria, and preferred supplier decisions.

Fourth, connect the systems.

This is where many organisations will struggle. Product carbon data needs to move across ERP, procurement, finance, product lifecycle management, compliance, supplier platforms, and digital product passport infrastructure. If the data cannot move, it cannot matter.

Fifth, be careful with AI. AI agents can help scale product carbon footprinting, compliance checks, emissions factor mapping, and documentation. Stephen described how AI capabilities could move companies from manually managing handfuls of emissions factors to scaling across tens of thousands of products. That is powerful.

But humans remain accountable. Stephen was clear on this too: AI agents can assist, but they cannot be accountable for decisions.

The strategy is not “let AI solve sustainability.”

The strategy is: give AI decision-grade sustainability data, strong governance, clear constraints, and human accountability.

The transition is already happening.

CBAM is live. Product passports are being built. Battery rules are moving from aspiration to evidence. Packaging is becoming a compliance system. Deforestation-free proof is becoming a market requirement. Forced labour rules will put human rights evidence into product eligibility.

This is not a far-off future. It is a staggered rollout of commercial reality.

The signal of change is also visible in how business leaders now talk about climate. Stephen noted that climate has moved from a niche sustainability-team topic, through an era of ambition, into a phase focused on the economics of carbon, risk exposure, and investor relevance.

That tracks with what I am seeing too.

The serious conversations are no longer about whether sustainability matters. They are about how to make it operational. How to measure it properly. How to use it in procurement. How to price risk. How to make product-level carbon data trustworthy enough for investors, customers, regulators, and AI systems.

This is the real story.

Sustainability is leaving the PDF.

It is entering the transaction.

And that is good news, even if it feels uncomfortable. Because once climate data becomes part of how products are designed, sourced, financed, priced, and sold, it stops being a communications exercise and starts becoming a lever for emissions reduction.

Back to where we started.

A few years ago, bad carbon data meant a weak report.

Increasingly, bad carbon data may mean a weaker product, a weaker supplier position, a weaker investment case, or a blocked market opportunity.

That should concentrate minds.

But it should also energise us. Because the companies that get this right will not just comply better. They will compete better. They will build cleaner supply chains, more resilient products, more credible claims, and smarter operating systems.

And that is exactly the kind of climate action we need now.

Practical.

Measurable.

Commercially real.

If you want to understand where this is heading, listen to my Climate Confident conversation with Stephen Jamieson of SAP Sustainability. It is one of those episodes that reframes the issue: carbon data is no longer just about reporting what happened.

It is becoming part of whether you get to sell what comes next.

Tags: Risk Management, Supply Chain, Sustainability

Bad Emissions Data Is Now a Supply Chain Risk

Bad Emissions Data Is Now a Supply Chain Risk

Here in Spain, olive oil has become a climate dashboard.

For years, it was just there. A kitchen staple. Drizzled on toast, poured over tomatoes, deployed with generous Mediterranean confidence. Then drought and heat hit production. Prices surged. In the first half of 2024, Reuters reported that Spanish households bought more sunflower oil than olive oil after olive oil prices soared after climate-driven production shocks.

That is climate risk in plain clothes.

Not abstract. Not theoretical. It is on the supermarket shelf. In household budgets. In procurement conversations. In margins.

This is where emissions data enters the story.

Once climate risk turns into food inflation, supply disruption, insurance exposure, financing cost, procurement risk, customer churn, employee disengagement, and investor scrutiny, a company’s carbon data stops being decorative. It becomes infrastructure.

Bad data is no longer harmless. Average data is no longer good enough. Missing data is not neutral.

In a recent episode of my Resilient Supply Chain podcast, Cynthia Lai made the point bluntly. If a company cannot provide credible emissions figures, banks and insurers may use proxy data or industry averages instead, potentially pushing the company into a higher-risk bucket with higher borrowing costs and insurance premiums.

The market fills in the blanks. Rarely with generosity.

That should make every board sit up. Emissions data is now about capital, insurance, tender eligibility, customer trust, recruitment, retention, brand credibility, and resilience.

The emissions problem is mostly hiding outside the walls of the organisation.

According to CDP and Boston Consulting Group’s 2024 analysis, corporate supply chain Scope 3 emissions were, on average, 26 times greater than direct operational emissions.

A quick translation. Scope 1 covers emissions from sources a company directly owns or controls. Scope 2 covers purchased electricity, heat, steam, or cooling. Scope 3 covers the rest of the value chain: purchased goods, transport, product use, waste, business travel, investments, and more.

In other words, the messy bit. So, naturally, the important bit.

The same CDP/BCG work found that upstream emissions from manufacturing, retail, and materials had a footprint 1.4 times total EU CO₂ emissions in 2022. Yet only 15% of disclosing companies had set a Scope 3 target.

That is not a data gap. It is a strategic blindfold.

CDP’s 2024 supply chain report also found that failure to address climate-related risks in supply chains costs nearly three times more than the actions required to mitigate them, while companies could unlock US$165 billion in potential financial gains from upstream climate-related opportunities.

The World Economic Forum and Boston Consulting Group have previously shown that eight supply chains, including food, construction, fashion, electronics, automotive, consumer goods, professional services, and freight, account for more than half of global emissions. They also estimated that decarbonising many end-to-end supply chains would add just 1–4% to end-consumer costs in the medium term.

That matters. The fossil economy has long framed low-carbon transition as uniquely expensive, while quietly offloading drought, flood, heat, health, conflict, volatility, and stranded-asset costs onto everyone else.

Regulation is catching up too.

In Europe, the Corporate Sustainability Reporting Directive, or CSRD, requires companies in scope to publish sustainability information using common European standards. The first companies applied the rules for financial year 2024, with reports published in 2025.

In California, the Climate Corporate Data Accountability Act, or SB 253, requires large US-based companies doing business in California to report Scope 1 and 2 emissions from 2026, and Scope 3 from 2027.

And then there is IFRS S2, the climate disclosure standard issued by the International Sustainability Standards Board. Put simply, it asks companies to disclose climate-related risks and opportunities that could affect cash flows, access to finance, or cost of capital.

That last phrase is the one to underline.

Access to finance. Cost of capital.

Not “nice sustainability story”. Money.

The first implication is financial.

Financed emissions are the greenhouse gas emissions linked to loans and investments. If a bank lends to a high-emitting company, those emissions become part of the bank’s own climate risk picture. Cynthia Lai explained this clearly on the podcast: banks are increasingly looking across their loan books and customer portfolios, adding emissions-related factors into risk assessment and credit scoring.

Insurers are doing something similar across insured operations.

Then there is PCAF, the Partnership for Carbon Accounting Financials, which develops greenhouse gas accounting standards for financial institutions. Its work helps banks, investors, and insurers measure emissions associated with loans, investments, and insurance. In plain English: your emissions may become someone else’s financial exposure.

Insurance-associated emissions are the emissions linked to what insurers cover. That sounds technical until a company finds its insurance renewal becoming more expensive, more conditional, or harder to secure.

As Cynthia put it, if you cannot get your operations insured, getting financing becomes much harder because banks like protection. There’s a sentence that should be stuck beside every procurement dashboard in Europe.

The second implication is commercial trust.

Customers increasingly want evidence, not slogans. PwC’s 2024 Voice of the Consumer Survey found that consumers said they were willing to pay an average of 9.7% more for sustainably produced or sourced goods, even with cost-of-living pressures.

Stated willingness is not the same as actual checkout behaviour. Anyone who has watched procurement knows the gap between intention and purchase can be wide enough to drive a diesel HGV through.

Still, customers are asking sharper questions. Weak emissions data makes those conversations harder. Losing a tender because your numbers are vague, unverifiable, or built on lazy averages means higher cost of sales, more procurement friction, and more work to win the next customer.

Retention matters too. Existing customers do not want to carry your climate uncertainty inside their Scope 3 inventory. If you cannot give them credible data, a competitor who can may suddenly look far more attractive.

The same logic applies to talent.

Deloitte’s sustainability research, reported in 2025, found that 63% of employees surveyed globally did not think their employers were doing enough on climate and sustainability, and 21% had considered changing jobs to work for a more sustainable company.

Intent does not always become action. Mortgages exist. Children eat. Careers are complicated.

But employer brand is now part of the climate credibility equation. Skilled people are expensive to recruit, replace, and train. If a company says climate matters but cannot produce credible emissions data, that gap can become a recruitment problem, a retention problem, and eventually a cost problem.

Investors are watching too. EY’s 2024 Global Institutional Investor Survey found that 36% of investors were dissatisfied with company progress on nonfinancial reporting, especially the materiality, comparability, and accuracy of sustainability data. Those are capital allocation words.

The first strategy is simple: move from averages to primary data.

In another Resilient Supply Chain conversation, John Beath defined primary data as data from the supplier actually making the product or material, rather than generic database averages or published studies. That means asking basic questions. What are the materials? How much do they weigh? Where did they come from? How were they transported? What energy was used? What waste was generated? What process created them?

This is not glamorous work. But it is where the truth lives.

The second strategy is to look where the carbon is, not where the optics are.

John gave a striking example of a company that had worked hard to remove styrofoam cups from a huge office site, while a tiny thermostat change would have had vastly greater impact. Visibility is a terrible proxy for materiality.

Corporate sustainability has a weakness for symbolic gestures. Cups. Posters. Reusable tote bags. Bamboo cutlery. The theatre is seductive. The carbon often sits elsewhere: raw materials, process heat, refrigerants, freight, product use, waste, supplier electricity, aluminium, cement, steel, plastics, packaging, returns, and end-of-life treatment.

John also described a solar panel manufacturer that assumed silicon was the main footprint problem, only to discover the aluminium frame was the real hotspot. Switching frame material cut the product footprint in half.

Measure first. Moralise later.

The third strategy is supplier segmentation.

Start with the top 20% of suppliers likely driving 80% of emissions. Use spend data if that is all you have. Use industry averages as a first screen, not the final answer. Build a heat map. Identify hotspots. Engage critical suppliers. Ask for primary data. Run pilots. Document improvement plans. Bring banks and insurers into the conversation before they bring you into theirs.

Cynthia Lai recommended exactly this pragmatic 80/20 approach, because perfect data delayed for years is just another form of inaction.

The fourth strategy is to embed carbon into decision systems.

Procurement. Product design. Enterprise resource planning systems. Supplier onboarding. Freight routing. Contract renewal. Capital approvals. Product lifecycle management. Board dashboards.

Carbon data cannot live in a sustainability side-file, updated annually, with a prayer and a pivot table. It has to show up where decisions are made.

Interestingly, the purchase order may become one of the most important climate tools in the enterprise. Not the glossy sustainability report. The purchase order. If it carries product carbon data, supplier energy mix, recycled content, logistics mode, and assurance status, it becomes a quiet machine for cutting emissions at scale.

AI can help too. It can classify supplier risk, detect anomalies, summarise regulation, spot missing data, prioritise supplier engagement, and map emissions hotspots. But it cannot magically convert poor data into truth. Bad data plus AI is still bad data, only now it arrives faster and with more confidence.

Capital is already moving.

The International Energy Agency’s World Energy Investment 2025 report estimated global energy investment at US$3.3 trillion in 2025. Around US$2.2 trillion was set to go to renewables, nuclear, grids, storage, low-emissions fuels, efficiency, and electrification, twice the US$1.1 trillion going to oil, gas, and coal.

The clean technology transition is not waiting for perfect consensus. It is being driven by economics, energy security, industrial strategy, customer demand, policy, and climate necessity.

Emissions data is becoming the accounting layer beneath that shift.

And the next frontier is already visible: financed emissions, insurance-associated emissions, facilitated emissions, and, very likely, enabled emissions.

Enabled emissions are the emissions made possible by a company’s products, services, technology, or expertise. Think of an AI system, software platform, consultancy, engineering service, or advertising campaign that helps expand fossil fuel production or high-carbon consumption. The concept is still developing, but the logic is clear. If your business helps others emit more, eventually someone will ask you to account for that.

That question may come from regulators, investors, customers, employees, insurers, banks, or all of them, because apparently civilisation occasionally enjoys sending reminders in bulk.

A bottle of olive oil does not care about your emissions factor.

It responds to heat, rain, soil, water, labour, logistics, energy, and markets.

So does business.

Accurate emissions data is not about pleasing regulators. It is about seeing the system clearly enough to act before the system acts on you.

Customers want credible claims because their own supply chain data depends on yours. Employees and potential employees want evidence because they are deciding where to spend their time, skills, and credibility. Boards want risk clarity. Investors want comparable information. Banks want credit signals. Insurers want exposure data. Policymakers want accountability. Suppliers need direction and support.

The organisations that win will not be the ones with the prettiest averages. They will be the ones with the best primary data, the clearest hotspots, the strongest supplier engagement, and the courage to move capital from carbon-heavy inertia into cleaner, cheaper, more resilient systems.

Measure first. Then act. Then prove it.

That is how we cut emissions without cutting through credibility. And it is how supply chains become not just cleaner, but stronger.

Photo credit Esencia Andalusí on Flickr

Tags: Climate Change, Supply Chain, Sustainability

Ireland’s Nuclear Power Debate Has a Grid Problem

Ireland’s Nuclear Power Debate Has a Grid Problem

I still remember the iodine tablets.

Not taking them. Just knowing they were there.

In drawers. In presses. In Fridges. In kitchen cupboards around the country. Small packets of official anxiety, sent to Irish households in 2002 in case of a major nuclear accident abroad. The Department of Health later confirmed that Ireland was the only country to issue iodine tablets to every household at the time. Nothing says “energy policy” quite like posting thyroid medication to the nation.

I write this as an Irishman, but not as someone living in Ireland. I have lived in Spain since 2008. So this is not a domestic “we should” argument. It is the view of an interested outsider looking in. Irish by birth. Energy analyst by trade. Slightly exasperated observer by long experience.

And now nuclear is back in the Irish conversation.

Recent commentary has argued that, with electricity bills high and renewable delivery lagging, the case for reopening Ireland’s nuclear power debate has never been stronger. It is a fair debate to have. Energy costs are painful. Grid constraints are real. Data-centre demand is politically and technically unavoidable. Ireland needs clean power, security, affordability, and resilience.

But reopening a debate is not the same as reaching the right conclusion.

And in the Irish context, domestic nuclear power still makes very little sense.

The strongest argument against nuclear in Ireland is not peak demand.

It is minimum demand.

EirGrid’s 2024 All-Island Transmission System Performance Report recorded a winter peak of 7,148 MW on 27 November 2024. That is the number nuclear advocates tend to point at. Big number. Serious face. Possibly a chart with a dramatic arrow.

But the more important number is the minimum summer night valley. In 2024, that was just 3,095 MW, recorded at 05:41 on 9 June. In 2020, it was even lower: 2,395 MW. That is the actual grid a nuclear plant would have to fit into. Not the political fantasy grid. The real one.

A conventional 1 GW reactor would represent roughly one-third of that low-demand period. Even smaller units would still be chunky in a small island system. Yes, nuclear plants can technically load-follow. But technical possibility is not the same as economic sense.

Nuclear economics depend on high utilisation. Build an expensive asset, then run it flat out for decades. That is the model. Turn it down because demand is low or wind is strong, and the capital cost does not politely disappear. It just gets spread over fewer megawatt-hours.

Ireland’s electricity challenge is not a lack of theoretical baseload.

It is flexibility.

Peaks. Troughs. Ramps. Wind surges. Wind lulls. Solar midday output. Evening demand. Interconnector flows. Battery cycles. Demand response. Dispatchable backup.

A large nuclear unit is not naturally suited to that system.

It is a fridge magnet in a clock mechanism.

There is another awkward question nuclear advocates need to answer.

What happens when the plant goes offline?

Nuclear reactors require planned outages for refuelling and maintenance. The US Energy Information Administration says nuclear plants typically refuel every 18 to 24 months, and that outages are usually longer than the refuelling itself because maintenance, upgrades, and repairs are carried out at the same time.

So if Ireland had a 1 GW reactor, the system would still need enough dispatchable capacity, storage, demand flexibility, and interconnection to cover the loss of that reactor when it was unavailable.

That is not a footnote.

That is the system cost.

In a large continental grid, losing a gigawatt is inconvenient. In a small island system, it is a major event. Nuclear does not remove the need for backup. It creates a large single contingency that the rest of the system must be built around.

So the real question is not simply: can nuclear supply clean power?

It is: can Ireland justify building a nuclear plant and then also building the parallel system needed for the days or weeks when that plant is offline?

Because that is what reliability requires.

Physics, tragically, does not care about op-eds.

New nuclear is slow.

Really slow.

Hinkley Point C in the UK was once expected much earlier and is now delayed into the 2030s, with EDF’s 2024 update putting expected cost at up to £35bn in 2015 prices. That is before translating the lesson into Irish political, regulatory, and planning conditions, where optimism often goes to be mugged by a judicial review.

Lazard’s 2025 Levelized Cost of Energy analysis puts new nuclear in the US at roughly $141–220/MWh. Utility-scale solar sits around $38–78/MWh, onshore wind around $37–86/MWh, utility solar plus storage around $50–131/MWh, and onshore wind plus storage around $44–123/MWh. These are not Ireland-specific project bids, but they are a useful benchmark from a widely cited financial analysis.

Now add time.

A nuclear plant in a country with no civil nuclear generation sector, no domestic nuclear regulator, no supply chain, no operating skills base, no waste pathway, and no site would not be a 2030 solution. It would be a 2040s bet, at best.

By contrast, solar, wind, storage, interconnection, demand response, and grid upgrades can be delivered in increments. Utility-scale solar can often be built in 6–12 months once consented and grid-connected. Battery projects are modular and can also be delivered far faster than nuclear. Onshore wind is slower, especially through planning and grid connection, but the construction phase is typically measured in months to a couple of years, not decades.

So the practical comparison is not nuclear versus candles.

It is nuclear versus portfolios: solar, wind, storage, interconnection, demand response, grid reinforcement, flexible backup, and smarter large-load management.

That portfolio can learn. It can adapt. It can fail partially without bankrupting the national strategy.

Nuclear is more binary.

And more expensive when it goes wrong.

Ireland’s data-centre electricity demand is astonishing. The Central Statistics Office reported that data centres consumed 22% of metered electricity in 2024, up from 5% in 2015. Consumption rose from 6,335 GWh in 2023 to 6,969 GWh in 2024.

But the data-centre debate is too often framed lazily.

Data centres are not automatically villains. I say that as a former developer of an Irish data centre, CIX.ie, in Cork. The issue is not whether data centres exist. They do. They are part of modern digital infrastructure. The issue is whether they behave like passive loads or active grid assets.

A data centre that demands power 24/7, ignores grid stress, and points to corporate PPAs as a moral fig leaf is part of the problem.

A data centre that can shift load, reduce demand when requested, support local constraints, co-locate with renewables, contract storage, provide flexibility, and participate properly in demand-side response can be part of the solution.

Ireland’s Large Energy Users policy is at least moving in that direction. The CRU’s 2025 decision assumes data centres procuring renewable energy equivalent to 80% of annual demand in its illustrative analysis, and the broader policy direction is clear: large loads need to contribute to the system, not simply lean on it.

That is the right framing.

Not “ban data centres”.

Not “build nuclear for data centres”.

But: if large loads want grid capacity, they should help the grid.

That is not anti-business. It is basic engineering discipline.

Someone will now mention small modular reactors.

They always do.

SMRs are the favoured escape hatch in modern nuclear debates because they sound like nuclear without the inconvenient bits: smaller, repeatable, factory-built, safer, cheaper, faster. A reactor you can order like a prefab kitchen, presumably with a tasteful backsplash and a twenty-year licensing process.

The problem is that commercial SMRs are still unproven.

The IEA says global nuclear capacity stayed flat in 2025: 3 GW of new nuclear came online, but that was offset by 3 GWof retirements, leaving global nuclear capacity at 420 GW. Construction started on 12.2 GW of nuclear in 2025, mostly in China and Russia. Interesting, yes. A bankable Irish electricity strategy? No.

Ireland would still need legislation, regulation, siting, emergency planning, waste management, security, skills, finance, and public consent. The “small” in SMR refers to reactor size. It does not magically shrink institutional complexity.

At this point, building Irish energy policy around SMRs is not pragmatism. It is delay when urgency is what is required.

Ireland might as well wait for other myths like fusion, cheap green hydrogen, or unicorn farts with grid-forming inverter capability.

The stronger Irish pathway is not mysterious.

Build the grid. Faster. More lines. More substations. More digital control. More connection capacity. More political honesty about the infrastructure required for electrification.

Accelerate renewables already in the pipeline. Ireland reached 8 GW of renewable electricity connected to the network in March 2026, according to ESB Networks and the Department of Climate, Energy and the Environment. That is not enough, but it is a real platform to build from.

Treat storage as core infrastructure. Batteries for short duration. Longer-duration storage for multi-hour and multi-day balancing. Thermal storage. Pumped hydro where feasible. Flexible demand. Clean dispatchable backup for rare events.

Use interconnection intelligently. Ireland does not need to own every generation technology domestically to benefit from system diversity. Interconnection with France gives access to a broader European electricity mix, including French nuclear, without Ireland taking on domestic nuclear siting, waste, construction, and political risk.

And make large loads earn their place. Data centres, hydrogen electrolysers, industrial heat, EV fleets, and other flexible demand should become grid partners, not just grid customers.

This is not anti-nuclear ideology.

It is pro-system realism.

Globally, the transition is moving.

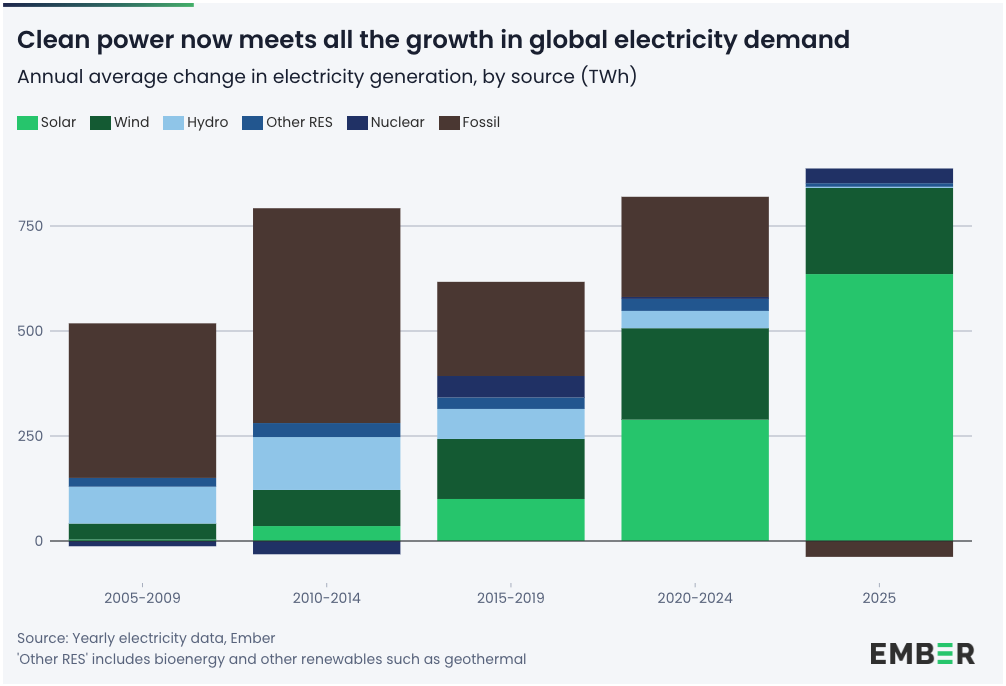

Ember’s Global Electricity Review 2026 found that clean electricity sources grew fast enough to meet all new global electricity demand in 2025, preventing an increase in fossil generation. Solar alone met 75% of the net increase in electricity demand, while solar and wind together met almost all of it.

Capacity additions tell the same story. IRENA’s Renewable Capacity Statistics 2026 reported that renewable power capacity increased by 692 GW in 2025, including 511 GW of solar and 159 GW of wind.

One set of technologies is scaling by the hundreds of gigawatts per year.

Nuclear is fighting to add single digits net.

That does not mean nuclear is useless globally. It does mean it is a strange place for Ireland to put scarce political, financial, regulatory, and planning capacity.

Ireland’s energy problem is urgent. High prices hurt households. High prices hurt businesses. Fossil fuel exposure hurts energy security, and resilience. Slow grid buildout hurts everything. But urgency is not an excuse to choose the slowest available tool.

Nuclear in Ireland sounds serious because it is large, expensive, centralised, and wrapped in engineering mystique.

But seriousness is not measured in concrete volume.

It is measured in fit.

And domestic nuclear does not fit Ireland’s grid, demand shape, political history, planning reality, delivery timeline, outage risk, or near-term climate needs.

Back to those iodine tablets.

They were a symbol of fear. But also a reminder that energy choices carry long shadows. Ireland has enough experience with imported risk, fossil volatility, and infrastructure delay to know better than to chase a technology whose best-case timeline belongs to the 2040s.

The better future is already visible.

Wind. Solar. Storage. Interconnection. Flexible demand. Smarter data centres. Electrified heat and transport. A stronger grid. More local generation. Less exposure to imported fuels.

Ireland does not need nuclear to be serious about energy.

It needs to build the clean, flexible, resilient electricity system that actually matches the island it is.

Urgently.

And with a little less faith in magic reactors.

This piece was originally published on TomRaftery.com. Photo credit IAEA Imagebank

Tags: Energy, Renewable Energy, Sustainability

Oil Shocks Make Electrification a Business Imperative

Oil Shocks Make Electrification a Business Imperative

I was looking at fuel prices the other day and thinking about how absurd this still is.

A conflict thousands of kilometres away. Tankers delayed. Insurance costs rising. Traders getting jumpy. And suddenly that ripples into household bills, freight costs, food prices, and boardroom planning across Europe and far beyond. That is the basic indignity of fossil fuel dependence. It hands immense power to events you cannot control, in places you do not govern, through systems you did not design.

That is the real lesson from the US-Israel war on Iran.

Reuters reported that IEA Executive Director Fatih Birol believes it could take around two years overall to restore the energy output lost in the Middle East conflict, while warning that markets may be underestimating the consequences of a prolonged closure of the Strait of Hormuz. In the UK, Ed Miliband’s response has not been to pretend that more North Sea drilling will somehow magic away global price volatility, but to argue for faster solar deployment, stronger EV uptake, and reforms to reduce the grip of gas on electricity prices. That is not ideological theatre. It is the beginning of a more realistic security doctrine.

The important point, though, is this: the war did not create the clean energy transition. Solar was already scaling. EVs were already getting cheaper. Batteries were already moving down the cost curve. Electrification was already spreading into buildings, transport and industry. What the war has done is expose, once again, how brittle the fossil system remains, and why the alternatives now look less like moral preference and more like strategic common sense.

The IEA’s Global Energy Review 2026 released this morning, is striking for what it confirms and for what it does not say. Global energy demand rose by 1.3% in 2025, slower than in 2024. Electricity demand, however, grew by around 3%, more than twice as fast. Solar PV was the single biggest contributor to the increase in global energy demand, accounting for more than 25% of the growth, the first time a modern renewable source has led global energy demand growth. Low-emissions sources together accounted for nearly 60% of demand growth. That is not a symbolic shift. That is system-level movement.

On the power side, the numbers are stronger still. Renewables and nuclear together added more generation than the entire increase in global electricity supply in 2025. Solar alone posted a record 600 TWh increase in generation, the largest annual increase ever recorded for any source outside post-crisis rebound periods. Renewable capacity additions hit 800 GW, while battery storage additions reached 108 GW, up 40% year on year. The direction of travel is unmistakable. But so is the caveat: fossil fuels still generated 57% of global electricity in 2025, with coal alone still the largest single source at 34%. This is acceleration, not completion.

Electric vehicles are following a similar arc. The IEA says electric car sales rose more than 20% in 2025 to 21 million vehicles, meaning roughly one in four new cars sold globally was electric. Its Global EV Outlook 2025 also found that first-quarter 2025 sales were up 35% year on year, with China projected to reach around 60% EV share of new car sales in 2025. In Europe, Reuters reported that BEV sales in the main markets surged 29.4% in the first quarter of 2026, helped by rising petrol prices after the war on Iran. That matters because it shows two forces working together: a structural cost and technology shift, and a geopolitical shock that makes oil dependence look even less attractive.

The affordability story is becoming harder to ignore. In the UK, Autotrader says new EVs are now cheaper to buy than petrol cars on average for the first time, at £42,620 versus £43,405, based on advertised prices after discounts and grants. That qualifier matters. This is not universal unsubsidised parity across every model and market. But it is still a meaningful milestone, particularly when paired with rising consumer interest. Autotrader says visits to its new-car platform were up 21% year on year in April. SMMT adds that March 2026 was the best month ever for UK BEV registrations, at 86,120. That is not a fringe market behaving politely. That is scale starting to show up in registration data.

The heavy-duty side of transport is also beginning to move, though this is where precision matters. Electrive reported that new energy heavy-duty trucks in China reached 54% of monthly new heavy-duty truck sales in December 2025, and 29% across the full year. But its source uses China’s NEV classification, which includes fully electric and certain plug-in drivetrains, and the article itself notes that subsidy phase-outs and anticipated tax changes distorted year-end buying. So this is not evidence that diesel is finished in trucking. It is evidence that even the difficult segments are starting to electrify faster than many assumed, once economics and policy begin to align.

The emissions story remains uncomfortable. Global energy-related CO2 emissions rose by around 0.4% in 2025 to a record 38.4 Gt. That is the part nobody serious should duck. Emissions did not fall globally. But growth slowed again, China’s emissions fell by around 0.5%, India’s were essentially flat, and the IEA estimates that clean technologies deployed since 2019 avoided around 3 Gt of CO2 in 2025 alone. So the more defensible conclusion is not “we’ve peaked”. It is that clean deployment is now materially suppressing fossil fuel demand and slowing emissions growth, and in several major markets the peak is either near or already behind them.

First, climate. The climate case remains brutal in its simplicity: the transition is happening, but not yet fast enough. Record solar growth is good. Record EV sales are good. Slower emissions growth is better than faster emissions growth. None of that changes the fact that 38.4 Gt is still 38.4 Gt. A critic is right to insist on that. But there is a difference between realism and fatalism. Realism says the transition must accelerate. Fatalism says the current progress does not matter because it is incomplete. That second argument is analytically lazy and politically dangerous.

Second, security. Fossil fuel security has always been overstated because it confuses access with sovereignty. If your country imports fuels priced on global markets and shipped through chokepoints vulnerable to war, blockade, sabotage or insurance shocks, you are exposed. Domestic clean power is not invulnerable, but it is much harder to embargo the wind, sanction the sun, or panic a battery with a tanker incident. That is why Miliband’s line about “clean energy security” resonates. It is not perfect. It is directionally right.

Third, affordability. IRENA reports that 91% of newly commissioned utility-scale renewable projects in 2024 delivered lower-cost electricity than the cheapest new fossil-fuel alternative, and that renewables avoided USD 467 billion in fossil fuel costs that year. BloombergNEF says average lithium-ion battery pack prices fell to USD 108 per kWh in 2025, while stationary storage pack prices fell to USD 70 per kWh. This does not mean every clean technology is cheap in every context. It does mean the cost trend is not moving in fossil fuels’ favour. And when wars shove oil and gas prices upwards, that advantage becomes more obvious, faster.

Fourth, resilience. This is where the critique bites hardest, and where leaders need to pay attention. Electrification is not a magic wand. It only works at scale with stronger grids, faster permitting, more storage, more flexible demand, better interconnection and more serious planning. The IEA’s Energy and AI work says data centres are set to account for nearly half of US electricity demand growth to 2030. Add EVs, heat pumps and industrial electrification, and the message is plain: the prize is huge, but the engineering challenge is real. The answer is not to retreat. It is to build the system that this new load profile requires.

For business leaders, the first strategy is to stop treating electrification as a CSR line item. It is a risk-management play. Fleets that electrify reduce exposure to oil-price swings. Buildings that shift to heat pumps and on-site solar reduce exposure to gas shocks. Companies that sign long-term clean power contracts are not merely polishing their brand. They are buying more predictable energy economics in a disorderly world.

For policymakers, the priority is system design, not slogan inflation. Faster grid build-out. Planning reform. Transmission investment. Storage support. Market rules that reward flexibility. Tariff structures that make electrification cheaper to use, not just cleaner to discuss. If governments want households and businesses to switch, the economics must be visible and the infrastructure must be there. Otherwise, the transition gets stuck between aspiration and irritation, which is where a lot of good ideas go to die.

For industry, the second strategy is to be honest about supply chains. Clean tech reduces one kind of dependency, but it can increase another if countries fail to diversify manufacturing, processing and grid equipment supply. So yes, push harder on domestic renewables, EVs, batteries and electrified industry. But also push on local and allied-country manufacturing, transformer supply, recycling, grid equipment, permitting capacity, and workforce development. Resilience means not swapping one bottleneck for another with a congratulatory press release attached.

The best evidence that something deeper is shifting is not rhetoric. It is investment and behaviour.

The IEA’s World Energy Investment 2025 says global energy investment is set to reach USD 3.3 trillion in 2025, with USD 2.2 trillion going to clean energy technologies and infrastructure, twice the USD 1.1 trillion going to fossil fuels. Consumers are moving too. The Guardian reports that Octopus has seen a 50% rise in solar sales and a 50% rise in heat pump sales since the latest Middle East conflict began, while March was the best month ever for EV sales in the UK. Again, that war did not create these trends. But it has made the old system’s weaknesses visible in a way that no white paper ever could.

That brings me back to the fuel-price board. To the family budget. To the logistics operator. To the minister trying to explain why violence abroad still whips through bills at home.

We should not have needed this many warnings. We should have moved earlier and faster. But the clean energy transition is no longer resting on climate ethics alone. It is now being pulled forward by the hard logic of security, affordability and resilience as well. That does not make the current moment good. It makes it clarifying.

So the strongest version of the argument is not that the war on Iran is somehow good news for energy. It plainly is not. It is that every fossil fuel shock now makes the case for electrification harder to evade. Solar is booming. EVs are scaling. Batteries are getting cheaper. Investment is shifting. Emissions are still too high, but the forces that can bend them down are becoming bigger, cheaper and more strategic with every passing year.

That is not victory. But it is movement. Real movement. Movement in the right direction. And in energy, that matters.

This article was first published on TomRaftery.com

Tags: Energy, Renewable Energy, Sustainability

Why Passive Cooling Matters More in a Hotter, More Volatile World

Why Passive Cooling Matters More in a Hotter, More Volatile World

Stand outside a warehouse in southern Spain at seven in the evening in August and you can feel the day still coming off the walls. The sun has eased. The heat has not. The building keeps radiating, the cooling system keeps working, and the meter keeps turning. It is an almost perfect metaphor for our energy system: we let heat build, spend too much fighting it, and then act surprised when the bill arrives looking like an insult.

That matters more now than it did even a few years ago.

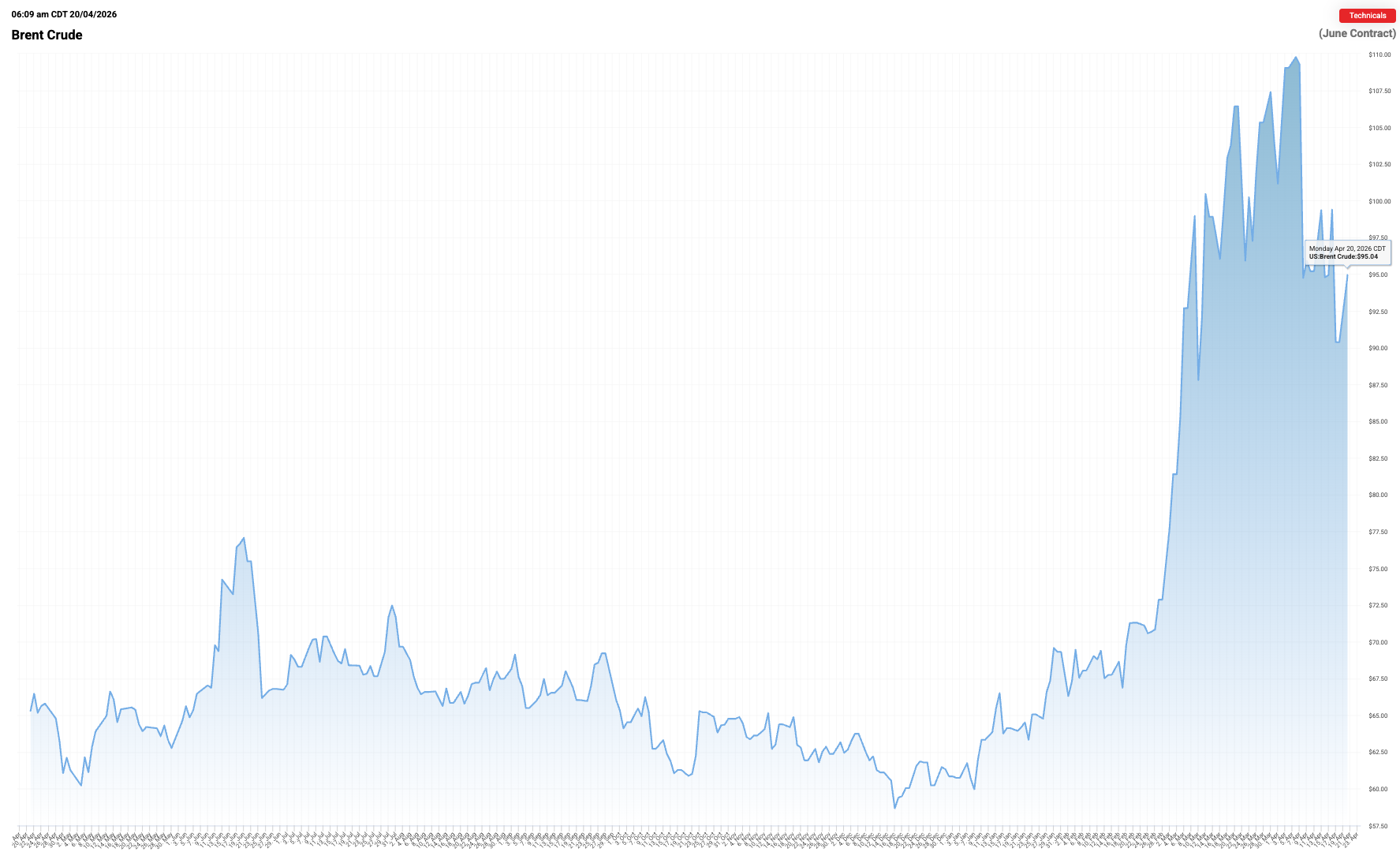

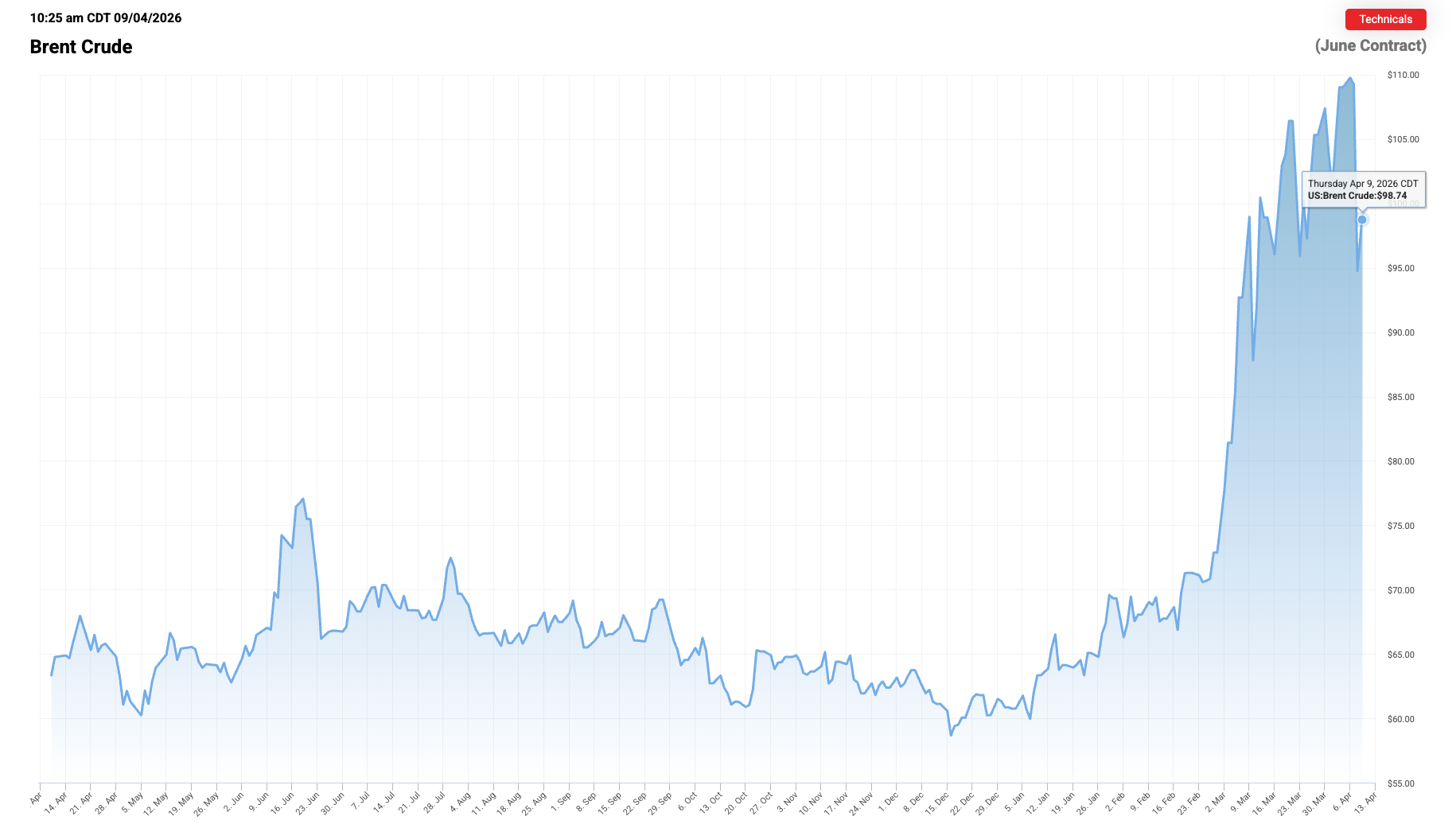

Heat is intensifying. Cooling demand is rising. Electricity systems are under more pressure. Data centres are expanding. And the war on Iran, alongside the disruption around the Strait of Hormuz, has reminded everyone that energy costs are still exposed to geopolitical shocks. Reuters reported this week that despite a fragile ceasefire, oil flows through Hormuz remained constrained, with Brent rebounding to around $98 a barrel and major supply disruption still in play.

That does not mean every building owner sees a straight line from Brent to their electricity bill. Markets are more complicated than that. But it does mean volatility is back in the foreground. Fuel insecurity, inflation pressure, grid stress, and energy cost uncertainty all rise together.

Which is why passive cooling deserves far more attention than it gets.

Not as a miracle cure.

Not as a substitute for all mechanical cooling.

But as one of the most practical, underused ways to cut cooling loads, reduce emissions, improve resilience, and protect operating margins.

The International Energy Agency has been warning for years that cooling is becoming one of the defining energy challenges of this century. In The Future of Cooling, the IEA said that without stronger efficiency action, energy demand for space cooling will more than triple by 2050. It also described cooling as the fastest-growing use of energy in buildings.

That trend has not gone away. It is accelerating.

The IEA’s 2026 electricity outlook says global electricity demand is set to grow strongly through 2030, driven by industrial electrification, electric vehicles, higher air-conditioning use, and the expansion of data centres and AI. Its 2025 Energy and AI analysis adds more texture: data centres account for around one-tenth of global electricity demand growth to 2030, but air conditioning in homes and offices contributes an even larger share.

That is the first key point. Data centres matter. AI matters. But ordinary cooling demand is still enormous, and still under-discussed.

The climate backdrop is equally clear. The WMO says Europe is the fastest-warming continent, and 2024 was Europe’s warmest year on record. The WHO says heat causes around 489,000 deaths globally each year, with 36% of those in Europe, and estimates that Europe saw 61,672 heat-related excess deaths in the summer of 2022 alone.

Heat is not a comfort issue with a sustainability footnote. It is already a public-health, labour-productivity, infrastructure, and energy-system issue.

Urban form makes it worse. A 2023 Nature Communications paper found that urban heat island effects in European cities are associated with economic impacts averaging about €192 per adult urban inhabitant per year. Higher temperatures do not just make cities uncomfortable. They also correlate with increased same-day respiratory hospitalisations.

The physical logic is straightforward. Buildings, roads, and hard surfaces absorb heat. Dark roofs absorb more. Poor envelopes admit more. Bad urban design traps more. Then we spend money moving that heat around mechanically.

The obvious implication is affordability. If a building gains less heat, it needs less active cooling. That can cut energy use, reduce peak demand charges, and sometimes defer or shrink HVAC investment. In warehouses and large commercial buildings, that matters a lot because cooling loads are often highly coincident with expensive peak periods.

But the stronger argument is not just cost. It is exposure.

Passive cooling reduces exposure on four fronts at once.

Heat.

Less solar gain means lower indoor temperatures, fewer hotspots, and, in some settings, better worker comfort and productivity. This is especially important in settings where heat directly affects health, comfort, and productivity, from warehouses to schools, hospitals, and lower-income housing.

Energy price volatility.

Again, not because oil prices directly set every cooling bill, but because lower cooling demand means lower dependence on volatile energy inputs overall. In stressed systems, demand reduction is often the cheapest hedge.

Grid stress and outages.

A passive measure keeps doing its job when nothing mechanical is running. That is valuable during heatwaves, curtailments, equipment failures, or outage events.

Emissions.

Even as grids decarbonise, wasted electricity is still waste. IRENA reported that 91% of newly commissioned utility-scale renewable capacity in 2024 produced electricity more cheaply than the cheapest fossil alternative. That is excellent news. But cheap clean electricity is not an excuse to ignore inefficient building envelopes. It is a reason to pair better supply with smarter demand.

And passive cooling is one of those rare climate measures that helps whether your motivation is cost, comfort, resilience, or emissions. Usually policy fights begin because people only agree on one of those. Here, the overlap is the point.

Passive cooling is not a single technology. It is a family of strategies: reflective roofs, radiative coatings, shading, insulation, thermal mass, natural ventilation, envelope sealing, landscaping, green roofs, and more. They do not perform equally everywhere.

A reflective roof may be a superb retrofit in Seville, Phoenix, or parts of India. It may have a weaker case in a much cooler climate where winter heating penalties matter more. Natural ventilation can help in some conditions but can be ineffective in hot, humid climates. Green roofs can reduce heat but may increase water demand and humidity, which is awkward in arid regions where water scarcity is already the problem.

That does not weaken the case for passive cooling. It makes the case more credible.

The right question is not, “Does passive cooling work?”

The right question is, “Which passive cooling measures make sense for this asset, in this climate, with this load profile, under this tariff structure?”

Serious operators should insist on that level of specificity.

The strongest use case for passive cooling is not where active cooling disappears. It is where active cooling becomes smaller, cheaper, and easier to run.

Warehouses are an obvious example. Large roof areas. Big solar exposure. Often uneven occupancy. Often poor thermal performance.

Data centres are more nuanced. No serious person is proposing that a reflective roof replaces precision cooling for high-density compute. But that is not the point. Roof reflectivity, insulation, airtightness, thermal-bridge reduction, and envelope analytics can reduce external heat gain and therefore reduce the burden on mechanical cooling systems.

That matters more as compute demand rises. The IEA’s AI work suggests data-centre load growth is material to electricity demand growth through 2030. So shaving cooling demand at the envelope level is not glamorous, but it is rational.

Hospitals, schools, airports, logistics facilities, social housing, and rail infrastructure also deserve more attention here. The common thread is simple: where heat gain is significant, occupancy matters, and cooling costs are meaningful, passive measures deserve a place in the stack.

First, stop treating cooling purely as an HVAC discussion.

Make it a demand-reduction and resilience discussion. Ask where heat is entering the asset before asking which bigger machine to buy.

Second, audit the building envelope.

Roofs, walls, glazing, insulation, air leakage, shading, and thermal bridges are not sexy, which in corporate terms usually means they are ignored until they get expensive.

Third, prioritise low-disruption retrofits.

Reflective roofs and coatings, shading, sealing, and selective insulation upgrades can often be implemented faster and with less operational disruption than deep structural interventions. That is especially relevant when capex is tight.

Fourth, model asset-specific economics.

The business case depends on climate, energy prices, operating hours, roof condition, existing HVAC performance, and whether the organisation owns the asset long enough to capture the savings. The payback may be compelling. It may also be mediocre. Better to know.

Fifth, treat passive and active cooling as complements.

The smartest cooling strategy is layered: reduce heat gain first, then optimise active systems, then align both with cleaner power and smart controls.

Sixth, connect cooling to urban and policy strategy.

Cities are starting to respond more explicitly. One sign of that is the emergence of Chief Heat Officers in places like Miami-Dade, Los Angeles, Phoenix, Athens, and Freetown. Whether or not that exact governance model spreads everywhere, the broader signal is clear: heat is becoming a planning issue, a public-health issue, and a policy issue, not just a private facilities issue.

What is changing is not the physics. White and reflective surfaces have been used for centuries. Buildings have always had envelopes. Shade has always existed. Humans are late to many obvious ideas, usually because quarterly reporting gets in the way.

What is changing is the context around them.

Heat is worsening.

Cooling demand is rising.

Electricity demand is growing faster.

Energy volatility is back.

Data-centre expansion is real.

And business leaders are finally being forced to think about adaptation and operating resilience in the same breath as decarbonisation.

That is why passive cooling is moving up the agenda.

Not because it is trendy.

Because the alternatives are increasingly expensive, exposed, and brittle.

Back to that warehouse roof in the evening heat. The point is not that passive cooling solves everything. It does not. The point is that too many organisations are still trying to solve a heat-gain problem with an equipment-only mindset. They are treating the symptom while leaving the cause sitting there in full sun.

That is starting to look less like normal practice and more like outdated thinking.

Passive cooling will not replace chillers, precision cooling, or smart active systems. It should not. But it can reduce how hard they work, how much energy they use, how vulnerable they are to price spikes and grid stress, and how much carbon they drag behind them.

That is not niche.

That is operational intelligence.

And in a hotter, more electrified, more volatile world, operational intelligence is going to matter a lot more than yet another glossy net-zero slide.

Passive cooling sits at the intersection of climate, affordability, resilience, and energy security, which is precisely why it deserves more strategic attention than it gets.

If you want to go deeper into the commercial reality behind this, including why sustainability alone rarely sellsy and why ROI still decides adoption, listen to my full conversation with Rob Atkin on the Climate Confident podcast. The most useful climate solutions are often the least theatrical. Passive cooling is one of them.

This article was originally posted on TomRaftery.com

Photo credit richard gadget on Flickr

Tags: Climate Change, Energy, Sustainability

Why the Strait of Hormuz Proves Renewables Are Strategic

Why the Strait of Hormuz Proves Renewables Are Strategic

A tanker does not need to explode for society to feel the blast.

Sometimes the shock arrives more quietly. First as a flicker on a trading screen. Then as a higher diesel bill. Then as fertiliser prices creep up. Then as freight rates jump, airline margins compress, central banks hesitate, and every executive who thought energy was “someone else’s problem” discovers, once again, that it sits underneath nearly everything.

We have seen this film before. In 2022, Russia’s invasion of Ukraine turned fossil fuel dependence into an invoice. Europe paid in inflation, industrial pain, and a frantic scramble for alternatives. Now, in 2026, the US-Israeli war on Iran is doing something similar. Different geography. Same basic lesson. When a large share of the global economy runs on fuels that must be dug up, loaded, insured, sailed through chokepoints, and defended by navies, the system is not strong. It is brittle.

And brittle systems fail noisily.

The Strait of Hormuz handles about one-fifth of global oil flows. This week, Brent has been heading for its steepest weekly gain since Russia’s full-scale invasion of Ukraine in February 2022, with traders repricing risk, inflation fears returning, and markets wobbling as shipping through Hormuz has been severely disrupted. [1][2]

That matters everywhere. But it matters especially in Asia. And over the longer arc, it matters particularly for China.

Because for all China’s immense industrial power, manufacturing heft, and recent progress in electrification, it still relies heavily on imported oil and gas moving through vulnerable seaborne routes. It has buffers, yes. Serious ones. But a buffer is not the same thing as immunity.

The deeper point is larger than China, or Iran, or this week’s oil chart. It is this: sunshine and wind do not need to transit Hormuz. Electrons generated at home do not require tanker insurance. Batteries do not panic when missiles fly over a shipping lane.

That is not environmental romanticism. It is hard-headed strategic logic.

Start with the immediate shock.

Reuters reported on 6 March 2026 that Brent crude had risen 17.2% this week, its biggest weekly jump since February 2022, as the conflict widened and disruptions around the Strait of Hormuz intensified. The strait is a chokepoint for about 20% of global oil flows. [1] Other reporting this week has underlined the same pattern: oil and gas prices have spiked, equity markets have fallen back, and fears of a renewed inflation shock have quickly returned. [2][3]

This is not merely a market story. It is a systems story.

According to Columbia’s Center on Global Energy Policy, half of China’s oil imports and nearly one-third of its LNG imports transit the Strait of Hormuz. In 2025, China imported about half of its crude oil and almost one-third of its LNG from the Middle East. Using China customs data and tanker-tracking estimates, Columbia notes that China imported 4.9 million barrels per day of crude from key Middle Eastern suppliers in 2025, while Kpler estimates it also imported 1.38 million barrels per day from Iran, much of it disguised in customs reporting. [4]

China is not blind to this vulnerability. Quite the opposite. It has been stockpiling aggressively. Columbia says China had 1.39 billion barrels of oil in storage as of 2 March 2026, enough to cover roughly 120 days of net crude imports at 2025 levels. Reuters separately reported analysts estimating China’s reserves at around 900 million barrels, or just under three months of imports. [4][5]

So yes, China can ride out a short-to-medium disruption better than many assume. That matters. But it does not erase the strategic exposure.

Columbia also points out that China has far less flexibility on gas. About 30% of its LNG imports arrive via Hormuz, and if those flows are disrupted, its options in the short term are ugly: consume less or pay more. Neither is a mark of energy sovereignty. [4]

Kismet: while oil traders were sweating tankers this week, China’s power sector was quietly becoming harder to blockade. Official data show the country added more than 430 GW of new wind and solar capacity in 2025 alone, pushing total renewable capacity above 1,800 GW and taking renewables to more than 60% of installed power capacity. [6]

That is the strategic shift in one statistic.

Now layer in cost.

IRENA’s latest cost data are devastating for the old fossil logic. In 2024, 91% of newly commissioned utility-scale renewable capacity produced electricity more cheaply than the cheapest new fossil fuel-based alternative. Utility-scale solar averaged USD 0.043/kWh globally, 41% cheaper than the least-cost fossil alternative. Onshore wind averaged USD 0.034/kWh, 53% cheaper. Battery storage costs have fallen 93% since 2010, reaching USD 192/kWh in 2024. [7]

In other words, the cleaner option is now frequently the cheaper one. And, increasingly, the safer one too.

China’s own economics sharpen this further. IRENA reports utility-scale solar in China at USD 0.033/kWh and onshore wind at USD 0.029/kWh in 2024, both below global averages. Columbia notes that China plans to more than double its energy storage capacity from 73.8 GW / 168 GWh in 2024 to 180 GW / 450 GWh by 2027 (for context, 1GW is roughly the output of a typical nuclear reactor). [4][7][8]

So the world’s biggest manufacturing economy is telling us something with its capital allocation. Not through speeches. Through steel, silicon, copper, and batteries.

The first implication is brutally simple: fossil fuels are not just a climate liability. They are a macroeconomic instability machine.

Every time a war, embargo, blockade, or shipping scare hits an oil and gas corridor, the costs spill well beyond the energy sector. Transport costs rise. Food systems feel it through fertiliser and freight. Industry feels it through heat and feedstocks. Central banks get dragged into decisions they did not ask for. Reuters reported this week that investors have already pushed back expectations of rate cuts as higher oil prices revive inflation concerns. [9]

So when someone frames renewables purely as a green preference, they are missing the plot entirely. The real argument is that dependence on globally traded hydrocarbons imports volatility directly into the bloodstream of the economy.

The second implication is geopolitical.

China’s reserves mean it can absorb pain for a while. But reserves are a bridge, not a destination. Over the long term, a country that remains structurally dependent on seaborne oil and LNG moving through contested chokepoints is exposed to coercion, price spikes, and strategic distraction. Columbia’s conclusion is telling: this conflict is likely to reinforce Beijing’s push for greater energy self-sufficiency, including domestic supply and a continued transition away from fossil fuels. [4]

That has consequences for everyone else. If China doubles down further on solar, wind, storage, EVs, grid flexibility, and electrified industry as a response to Hormuz risk, it will not just reduce exposure. It will deepen its manufacturing lead in the very technologies the rest of the world also needs.

That should worry Western policymakers who still treat clean technology as a climate niche rather than an industrial strategy.

The third implication is moral as much as economic.

Wars keep revealing what the energy transition really is. It is not simply a matter of emissions accounting. It is an escape route from recurring hostage situations. Oil and gas dependence binds societies to supply chains that can be disrupted by autocrats, insurgents, sanctions, naval standoffs, and insurance markets having a nervous collapse. Renewable electricity, especially when paired with storage and flexible demand, localises a larger share of the energy system. It shortens the chain. It reduces the hostage risk.

Not perfectly. Minerals matter. Grids matter. Manufacturing concentration matters. But compare the two systems honestly. One depends on endless daily combustion fuel deliveries through geopolitical chokepoints. The other depends on building assets that then harvest local flows of energy for decades.

That is a meaningful difference.

First, electrify faster.

Transport, low-temperature heat, much of industry, and large parts of buildings should be pushed towards direct electrification wherever technically feasible. Every vehicle shifted from imported oil to domestically generated electricity weakens the power of a future chokepoint crisis. Every heat pump installed instead of a gas boiler cuts exposure to commodity spikes. Every industrial process electrified where possible reduces dependence on molecules that can be embargoed, bombed, or extorted.

Second, build storage and flexibility as strategic infrastructure, not optional extras.

Solar and wind without storage are useful. Solar and wind with storage, demand response, stronger interconnection, and modern grid operations are something else entirely. They become resilience assets. They turn variable generation into dependable systems capability. China’s push towards 180 GW of energy storage by 2027 is not some abstract climate gesture. It is a recognition that the grid of the future needs balancing muscle. [4][8]

Third, stop measuring energy security with 20th-century assumptions.

For too long, policymakers treated “security” as synonymous with stockpiles, pipelines, and military protection of sea lanes. Those still matter in the current system. But real 21st-century energy security also means rooftop solar, utility-scale renewables, batteries, transmission, digital grid controls, EVs, and flexible industrial loads. It means reducing the volume of fuels that must be imported in the first place.

The best barrel in a crisis is the one you no longer need.

Fourth, treat clean tech as industrial policy.

This is where Europe, in particular, still under-thinks the challenge. If renewables with storage are now cheaper than new fossil generation in most cases, and if they also improve security and resilience, then deployment speed becomes an economic competitiveness issue. Slow permitting, weak grid investment, and policy drift are no longer administrative annoyances. They are strategic self-harm.

The encouraging part is that this transition is already happening.